Filing a renter’s claim is not all that different than filing a homeowners claim. The key to both is advance preparation. So let’s rewind and discuss what you should do before damage happens. Once you have purchased homeowner’s insurance review the claim process with your agent. Most insurance companies provide information to the homeowner with instructions for filing a claim. Review this information and put it in a place where you can easily find it in case something does happen.

This is important because insurance companies all have different procedures. But they all have some things in common. First, file your claim as soon as possible. Delaying this step could lead to issues. So, if your insurance provider has a 24-hour hotline, call as soon as possible. This will put the claim wheels in motion and lead to a faster resolution.

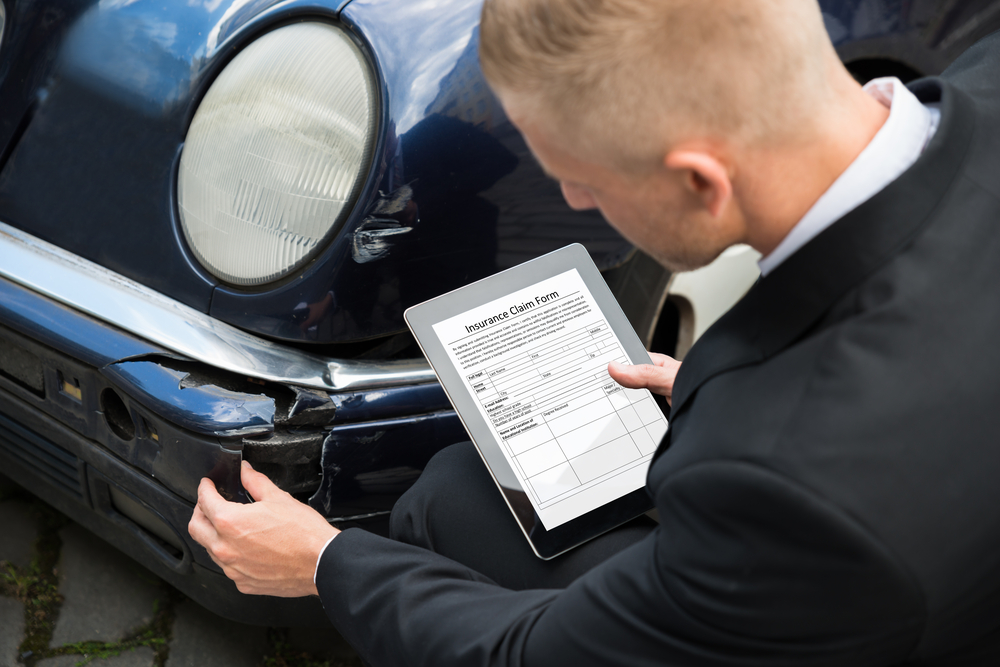

You will be assigned a claim number and agent. The claim agent may come to your home to assess that damage and ask for more details about the incident. Be prepared to have receipts or any supporting details that the claims agent asks for. The claims agent will assess the damage and help with the process of repairs. Often times claims agents have preferred vendors that will repair the damage. Using these preferred vendors often provides many benefits. They are generally very responsive, and they guarantee with work.

The more prepared you are before an accident occurs, the better prepared you’ll be to file a claim and provide the information required to process your claim. That means understanding the claims process for your insurance company. Review the process with your agent and ask questions. You’ll be glad you did.

To learn more about renters insurance and the claims process for your insurance carrier, contact your independent Provident Insurance agent. We serve Plainfield, Greenwood, Avon, Brownsburg, Indianapolis, Carmel, Zionsville and the entire central Indiana area. Stop in one of our convenient locations to discuss your insurance needs today.